Research ArticleOpen Access, Volume 2 Issue 4

Dynamics of Membership Attrition in Community-Based Health Insurance Programs: A Case Study from Amhara Region

Kebede Molla Melkamu*; Xu Mengmeng

School of Government, University of International Business and Economics, Beijing, Chaoyang District, China.

*Corresponding author: Kebede Molla Melkamu

School of Government, University of International Business and Economics, Beijing, Chaoyang District, China.

Email: mollamelkamu1974@gmail.com

Received : Sep 12, 2024 Accepted : Oct 15, 2024 Published : Oct 22, 2024

Epidemiology & Public Health - www.jpublichealth.org

Copyright: orgMelkamu KM © All rights are reserved

Citation: Melkamu KM, Mengmeng X. Dynamics of Membership Attrition in Community-Based Health Insurance Programs: A Case Study from Amhara Region. Epidemiol Public Health. 2024; 2(4): 1060.

Abstract

High dropout rates undermine the effectiveness of CBHI programs, prompting this study to investigate factors influencing membership retention. We conducted Kaplan-Meier survival Analysis (KMA), Weibull Accelerated Failure Time (AFT), and Inverse-Gaussian Shared Frailty Models using data from 772 respondents. The KMA showed that retention rates declined significantly after the second year, with survival probabilities dropping from 96.89% in the first year to 46.32% by the eighth year. Cox regression identified significant predictors of dropout, including “intention to renew membership (B=0.935, p< 0.001), perceived healthcare quality (fair: B=0.559, p=0.020; good: B=0.647, p=0.007), and service quality (satisfactory: B=0.279, p=0.092)”. The Weibull AFT with Inverse-Gaussian frailty distribution confirmed these findings, with the shape parameter (p=2.073) indicating an increasing hazard function over time and the best-fit model, achieving the lowest AIC (874.862) and BIC (963.169) values.

Keywords: Membership attrition; Program-specific variables; Survival analysis; Kaplan-Meier method; Cox regression; Weibull AFT model.

Introduction

Community-Based Health Insurance (CBHI) schemes provide financial protection against healthcare costs by pooling community resources, making healthcare more accessible and affordable for low-income populations, and improving overall health outcomes. CBHI programs leverage collective resources to distribute healthcare costs more equitably among members, enhancing their ability to access necessary medical services without significant financial burden based on the principle of risk sharing among the community of insured individuals to provide financial protection against the impoverishing effects of health expenditure [1-3].

Enrollment in most CBHI schemes is voluntary. Typically, premiums are low and independent of individual health status [4]. There is substantial evidence that being affiliated with CBHI schemes is associated with an increase in healthcare utilization and some evidence that such schemes provide financial protection in terms of reduced out-of-pocket spending [5-42], suggest that the insurance had limited effects on average out-of-pocket expenditures in the target areas but substantially reduced the likelihood of catastrophic health expenditure. Despite these benefits, initial uptake and renewal rates in CBHI schemes tend to be low. Consequently, these programs often need help with high dropout rates, undermining their sustainability and effectiveness [28,29]. Understanding the dynamics of membership attrition (dropout) is, therefore, critical for the success of CBHI programs.

Countries like India and Bangladesh have seen significant enrollment in CBHI schemes in Asia. However, retention remains challenging due to affordability, perceived quality of care, and administrative efficiency [11,5,6]. Due to economic disparities and health system inefficiencies, retention issues persist in Latin America, such as Mexico and Colombia [12]. CBHI programs are widespread in Africa, but their success varies significantly across countries. Studies in Ghana and Nigeria indicate that economic barriers, trust in the system, and health service quality significantly aggravate attrition rates [8,6]. In contrast, Rwanda’s CBHI program is often cited as a success story, with high enrollment and controlled attrition rates attributed to strong government support and community involvement [13]. However, sustainability remains a concern, particularly amid economic shocks and health system challenges.

Recent studies have emphasized the importance of program-specific factors in determining attrition from CBHI membership. Factors such as intention to renew membership, health status, distance to the nearest health center, community satisfaction, service quality, perceived healthcare quality, community participation, premium amount, and accessibility to healthcare services play significant roles in influencing an individual’s decision to remain enrolled in CBHI programs [8,5,6]. Previous studies in Ethiopia have highlighted economic stability, health literacy, and accessibility to health services as critical determinants of CBHI enrollment and attrition [10-14]. Additional barriers include economic instability, limited awareness about health insurance benefits, and variable quality of healthcare services [9,7,27]. Logistical challenges in premium collection and service delivery further complicate the retention landscape.

The dynamics of membership attrition in CBHI programs are complex and multifaceted [31], which is why previous research has highlighted several critical factors influencing attrition, including demographic characteristics, socioeconomic status, and program-specific variables [6]. While many studies have focused on enrollment and initial uptake of CBHI, there remains to be a significant gap in understanding the factors that drive membership dropout.

This study aims to examine the timing of attrition in CBHI programs and identify the factors contributing to this occurrence. The research employs various statistical techniques for analyzing survival data, including Kaplan-Meier Survival Estimation, Cox Regression, the Weibull Accelerated Failure Time (AFT) Model, and the Inverse Gaussian Shared Frailty Model. These methods uncover the underlying patterns of member dropout in CBHI programs.

Kaplan-Meier Survival Estimation is a widely used non-parametric method in survival analysis that estimates the probability of survival beyond a specific time point [15,39]. This approach generates a step function representing the survival probability at each event, making it especially useful for handling censored data. Censored data refers to cases where the event of interest (in this case, member dropout) does not occur within the study period. In CBHI programs, Kaplan-Meier curves can effectively depict member retention rates over time, highlighting critical periods with an increased dropout risk. For example, [20] employed Kaplan-Meier analysis to assess member retention in health insurance schemes, pinpointing crucial intervals where attrition is more likely to occur.

Cox Proportional Hazards Regression, commonly called Cox Regression, is a semi-parametric method used to model the hazard rate as a function of covariates. It enables the evaluation of the impact of multiple variables on the time of an event without requiring the specification of a baseline hazard function [17]. In the context of CBHI programs, Cox Regression is particularly beneficial as it identifies significant predictors of membership attrition, considering various Program specific and socioeconomic factors. For instance, research by [16] utilized Cox Regression to investigate the determinants of dropout in health insurance programs, demonstrating its effectiveness in highlighting key factors influencing member retention.

The Weibull Accelerated Failure Time (AFT) Model is a parametric approach to survival analysis that assumes a particular distribution for survival times. It models the logarithm of survival time as a linear function of covariates, providing insights into how these factors may accelerate or delay the time to an event [23]. The Weibull AFT Model’s capability to accommodate time-varying covariates and its adaptability in modeling different hazard shapes make it well-suited for CBHI studies. For example, [21] used the Weibull AFT Model to examine factors affecting the duration of enrollment in health insurance programs, identifying variables that significantly impact the timing of dropout.

The Inverse Gaussian Shared Frailty Model extends traditional survival models by incorporating random effects to account for unobserved heterogeneity among subjects. Frailty models posit that individuals within the same group share a common frailty, which affects their hazard rates [18]. In CBHI programs, the Inverse Gaussian Shared Frailty Model is beneficial for investigating group-level effects on membership attrition, such as premium amount, geographic location or community characteristics. Studies like those by [22] have employed frailty models to address unobserved heterogeneity in health insurance data, offering more profound insights into the factors influencing member behavior.

The integration of these methods facilitates a nuanced analysis of survival data, capturing the complexities of membership dynamics within CBHI programs. Building upon established research in the field, this study contributes to the broader literature on health insurance retention and sustainability. By identifying the factors contributing to attrition and the critical periods of increased dropout risk, this research provides evidence-based recommendations for enhancing CBHI programs, thereby contributing to the sustainability and effectiveness of health insurance schemes.

Methodology and analytical approach

This study aims to understand the factors influencing membership attrition in the Community-Based Health Insurance (CBHI) program by employing a comprehensive methodology and analytical approach. The primary dependent variable, “the time to membership attrition,” measures the total duration of participation in the CBHI program, from enrollment until dropout or renewal, providing a detailed view of membership continuity [51]. The failure variable, defined as the “decision to renew membership,” alongside the event variable, indicates whether a member has dropped out (coded as 2) or renewed membership (coded as 1 for censored), enabling precise identification of attrition events through survival analysis [44,33].

The study meticulously explores several independent variables, including Intention to Renew Membership, a categorical variable with levels Yes, No, and Undecided, coded as 1, 2, and 3, respectively, providing insights into commitment and potential dropout risks [43]. The Premium Amount is categorized into four bands ($13-19, $20-28, $28-38, and $39-57) and coded from 1 to 4, reflecting affordability and financial burden [55]. Distance to the Nearest Health Facility, measured in minutes (5-30, 35-60, and 70-180), is coded as 1, 2, and 3, assessing how geographical barriers impact retention rates [53]. Perceived Healthcare Quality, categorized as Poor, Fair, and Good, with coding from 1 to 3, captures care quality perceptions that influence program continuation [48]. Service Quality, assessed as Excellent, Satisfactory, and Poor, coded from 1 to 3, offers insights into areas where service improvements may reduce dropout rates [52]. Community Satisfaction with CBHI, categorized as Highly Satisfied, Moderately Satisfied, and Dissatisfied, coded from 1 to 3, plays a significant role in member retention [54]. Health Conditions of the Household, categorized as Poor, Fair, and Good, coded as 1, 2, and 3, examine how health needs impact program retention [45]. Community Participation in CBHI, categorized as Active, Some, and Limited participation, linked to retention rates and coded as 1, 2, and 3, along with the number of Household Members, categorized into 1-3, 4-6, and 7-10 members and coded from 1 to 3, explores the relationship between household size and CBHI program retention likelihood [46,49].

This study incorporates these variables to capture a comprehensive picture of factors affecting membership attrition, ensuring relevance, reliability, and validity, aligned with the study’s objectives to provide actionable insights for policymakers and program managers [47]. Data were collected using structured questionnaires with demographic questions and Likert scale items, capturing respondents’ socioeconomic status, health conditions, perceptions of the CBHI program, and reasons for attrition or dropout, with approval from the Amhara Region Public Health Institutes [31,33]. Data collection was conducted by 54 trained enumerators through face-to-face interviews from January to June 2024, ensuring data reliability and validity [35].

Analytical techniques, including Kaplan-Meier Survival Estimation, Cox Regression, the Weibull Accelerated Failure Time (AFT) Model, and the Inverse Gaussian Shared Frailty Model, were performed using STATA 17. The Kaplan-Meier method provided a non-parametric analysis of survival probabilities and attrition rates over time, highlighting critical periods of attrition. Cox Regression, a semi-parametric model introduced by Sir David Cox in 1972, explored the relationship between survival time and predictor variables, utilizing its ability to handle censored data, incorporate time-independent and time-dependent covariates, and offer insights into proportional hazards and the impact of specific covariates on membership dropout [17-50].

One of the critical characteristics of the Cox regression method is its ability to analyze complex survival data without requiring a specific baseline hazard function, allowing for flexibility in examining various factors affecting survival outcomes. The model also efficiently handles right-censored data, shared in survival analysis, where subjects may not experience the event of interest within the study period. The proportional hazards assumption, a vital feature of the Cox model, implies that the hazard ratios for covariates remain constant over time, simplifying result interpretation and enabling a straightforward analysis of the relative impact of covariates on the hazard rate [55].

The Weibull AFT Model incorporated covariates to understand the factors influencing membership attrition. At the same time, the Inverse Gaussian Shared Frailty Model accounted for unobserved heterogeneity, capturing latent factors affecting survival times, ensuring more accurate estimation of observed covariates’ effects, and guiding targeted interventions to enhance program sustainability and effectiveness [17-23].

Participants and sample size determination

The study included 772 respondents (610 current and 162 former members) purposefully selected from five administrative zones, 27 woredas, and 135 kebeles. To determine the sample size based on Cochran’s formula and considering a design effect for stratified sampling, a detailed calculation for a total population of 2,880,666 with five zones and a population per zone of 462,889 [32].

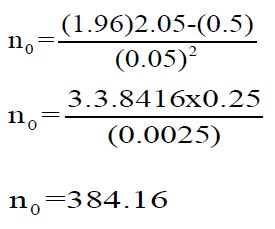

Step 1: Calculate the initial sample size using Cochran’s formula for sample size determination is:

n0= Z2p(1-p), Z2 .p.(1-p)/e2 where:n0 = initial sample size, Z=Z-value (the number of standard deviations from the mean corresponding to the desired confidence level, typically 1.96 for a 95%confidence level), p=estimated proportion of the population that has the attribute of interest(if unknown, use 0.5 for maximum variability), and e=desired level of precision (margin of error, typically 0.05 for 5% margin of error)

Using the common values: Z=1.96, p=0.5, e=0.05

So, the initial sample size (without considering the finite population and design effect) is approximately 384.

Step 2: Adjust for finite population

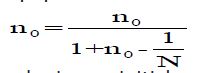

Since the population is finite, we need to adjust the sample size using the finite population correction:

n =adjusted sample size, n̥ =initial sample size, N= Population size, Using N=2,2880,666

So, the adjusted sample size for the finite population is still approximately 384.

Step 3: Apply the design effect

The design effect (DEFF) accounts for the increased variance in stratified sampling. A typical design effect is around 1.5 to 2. Let us use a design effect of 2 for this example.

Adjusted = n. DEFF, adjusted = 384.11.2, adjusted = 768.22

Thus, considering a design effect of 2, the final sample size is approximately 768.

Step 4: Allocate the sample size to different zones

Assuming proportional allocation based on the population of each zone:

nzone = 462,889/2,880,666 × 768.22, nzone = 123.48

So, the sample size for each zone is approximately 123 to 124 respondents.

Kaplan–Meier survival analysis of CBHI membership attrition

The Kaplan-Meier survival function analysis provides an overview of the attrition rates of CBHI members over eight years. The analysis begins with 772 at-risk members, with dropout (failure) and censored (renewal) events recorded annually.

Table 1: Kaplan–Meier survival analysis of CBHI membership Attrition.

| Time (Years) | At Risk | Dropout (Failure) | Censored | Survivor Function | Std. Error | 95% Confidence Interval |

|---|---|---|---|---|---|---|

| 1 | 772 | 24 | 87 | 0.9689 | 0.0062 | 0.9540-0.9791 |

| 2 | 661 | 24 | 49 | 0.9337 | 0.0093 | 0.9130-0.9497 |

| 3 | 588 | 44 | 101 | 0.8639 | 0.0133 | 0.8355-0.8877 |

| 4 | 443 | 40 | 89 | 0.7859 | 0.0169 | 0.7506-0.8168 |

| 5 | 314 | 31 | 81 | 0.7083 | 0.0201 | 0.6667-0.7457 |

| 6 | 202 | 17 | 49 | 0.6487 | 0.0231 | 0.6014-0.6918 |

| 7 | 136 | 21 | 70 | 0.5485 | 0.0280 | 0.4919-0.6015 |

| 8 | 45 | 7 | 38 | 0.4632 | 0.0379 | 0.3875-0.5354 |

Note: This table shows the Kaplan–Meier survival estimates for CBHI membership over eight years, indicating the number of members at risk, dropout events, censored events, survivor function, standard error, and 95% confidence intervals for each year.

In the first year, the survivor function is 0.9689, with a standard error of 0.0062 and a 95% confidence interval of 0.9540 to 0.9791. This indicates that 96.89% of the members remain in the CBHI program after the first year, showcasing initial solid retention. However, as time progresses, the survival probability declines. By the second year, the survivor function drops to 0.9337, with a standard error of 0.0093 and a 95% confidence interval of 0.9130 to 0.9497

A more pronounced decline is observed in the third year, where the survival probability decreases to 0.8639, with a standard error of 0.0133 and a 95% confidence interval of 0.8355 to 0.8877. This trend continues, with the fourth and fifth years showing survival probabilities of 0.7859 and 0.7083, respectively. The standard errors increase to 0.0169 and 0.0201, indicating growing variability in the attrition rates, and the confidence intervals widen accordingly.

In the later years, the probability of survival continues to decline. By the sixth year, the survivor function is 0.6487, with a standard error of 0.0231 and a 95% confidence interval of 0.6014 to 0.6918. The seventh year shows a further drop to 0.5485, with a standard error of 0.0280 and a confidence interinterval of 0.4919 to 0.6015. By the eighth year, the survival probability reaches 0.4632, with a standard error of 0.0379 and a confidence interval of 0.3875 to 0.5354.

The Kaplan-Meier analysis indicates that the retention rates of CBHI members are highest during the initial years, with a significant number of members remaining in the Program during the first and second years. However, retention significantly declines starting from the third year, with a more pronounced drop observed in the subsequent years. This suggests that members are likely facing challenges or changes in circumstances that lead to dropout as time progresses. The increasing standard errors and wider confidence intervals in the later years indicate more significant variability and uncertainty in the retention rates, suggesting that the factors influencing dropout become more pronounced or diverse over time. To improve retention rates, it is crucial to focus on the critical periods identified in the analysis, particularly between the third and fifth years.

Kaplan-Meier survival analysis of CBHI program-specific factors

By employing Kaplan-Meier survival analysis, the study evaluates the impact of various program-specific factors on the time to drop out among CBHI members. Understanding these factors is crucial for enhancing the sustainability and effectiveness of the CBHI program.

Table 2: Kaplan-Meier estimates for survival time CBHI program specific factors:(Defined event “Dropout,” Time “Total membership year”)

| Variables | Total N | N of Events (Dropout) | Censored (Renew) | Mean | 95%Confidence Interval | LogRank (Mantel-Cox) | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| N | Percent | Estimate | Std. Error | Lower Bound | Upper Bound | Chi-Square | df | Sig. | |||

| Intention to renewmembership | 62.796 | 2 | 0.000 | ||||||||

| yes | 368 | 51 | 317 | 86.1% | 7.158 | .110 | 6.942 | 7.374 | |||

| no | 188 | 88 | 100 | 53.2% | 5.499 | .190 | 5.128 | 5.871 | |||

| Undecided | 216 | 69 | 147 | 68.1% | 6.265 | .172 | 5.928 | 6.603 | |||

| Overall | 368 | 51 | 317 | 86.1% | 6.458 | .090 | 6.281 | 6.634 | |||

| Premium Amount | 2.916 | 3 | 0.405 | ||||||||

| 13-19$ | 202 | 58 | 144 | 71.3% | 6.458 | .175 | 6.115 | 6.800 | |||

| 20-28$ | 515 | 138 | 377 | 73.2% | 6.407 | .113 | 6.186 | 6.628 | |||

| 28-38$ | 39 | 7 | 32 | 82.1% | 7.089 | .314 | 6.474 | 7.704 | |||

| 39-57$ | 15 | 5 | 10 | 66.7% | 5.769 | .528 | 4.734 | 6.804 | |||

| Overall | 771 | 208 | 563 | 73.0% | 6.454 | .090 | 6.278 | 6.631 | |||

| Distance to nearesthealth facility | 4.629 | 2 | 0.049 | ||||||||

| 5-30 minutes | 319 | 86 | 233 | 73.0% | 6.393 | .142 | 6.115 | 6.672 | |||

| 35-60 minutes | 253 | 55 | 198 | 78.3% | 6.695 | .155 | 6.390 | 7.000 | |||

| 70-180 minutes | 200 | 67 | 133 | 66.5% | 6.291 | .175 | 5.948 | 6.635 | |||

| Overall | 772 | 208 | 564 | 73.1% | 6.458 | .090 | 6.281 | 6.634 | |||

| Perceived Healthcare Quality | 57.088 | 2 | 0.000 | ||||||||

| Poor | 385 | 55 | 330 | 85.7% | 7.101 | .110 | 6.886 | 7.316 | |||

| Fair | 176 | 80 | 96 | 54.5% | 5.600 | .196 | 5.216 | 5.984 | |||

| Good | 211 | 73 | 138 | 65.4% | 6.166 | .174 | 5.825 | 6.508 | |||

| Overall | 772 | 208 | 564 | 73.1% | 6.458 | .090 | 6.281 | 6.634 | |||

| Service quality of theCBHI program | 4.132 | 2 | 0.027 | ||||||||

| Excellent Quality | 282 | 68 | 214 | 75.9% | 4.652 | 6.586 | .150 | 6.291 | |||

| Satisfactory quality | 271 | 89 | 182 | 67.2% | 5.058 | 6.218 | .154 | 5.917 | |||

| Poor Quality | 219 | 51 | 168 | 76.7% | 4.647 | 6.634 | .163 | 6.313 | |||

| Overall | 772 | 208 | 564 | 73.1% | 4.790 | 6.458 | .090 | 6.281 | |||

| Community Satisfaction with the CBHIProgram | .562 | 2 | 0.755 | ||||||||

| Highly satisfied | 297 | 83 | 214 | 72.1% | 6.423 | .149 | 6.131 | 6.714 | |||

| Moderately Satisfied | 258 | 69 | 189 | 73.3% | 6.552 | .148 | 6.261 | 6.842 | |||

| Dissatisfied | 217 | 56 | 161 | 74.2% | 6.385 | .178 | 6.035 | 6.734 | |||

| Overall | 772 | 208 | 564 | 73.1% | 6.458 | .090 | 6.281 | 6.634 | |||

| Number Of Household Members | 3.371 | 2 | 0.018 | ||||||||

| 1-3 members | 266 | 82 | 184 | 69.2% | 6.261 | .157 | 5.953 | 6.568 | |||

| 4-6 members | 368 | 91 | 277 | 75.3% | 6.489 | .133 | 6.229 | 6.749 | |||

| 7-10 members | 138 | 35 | 103 | 74.6% | 6.719 | .198 | 6.332 | 7.106 | |||

| Overall | 772 | 208 | 564 | 73.1% | 6.458 | .090 | 6.281 | 6.634 | |||

| The health condition of the household members | .481 | 2 | 0.786 | ||||||||

| poor | 225 | 60 | 165 | 73.3% | 6.505 | .171 | 6.170 | 6.839 | |||

| Fair | 346 | 92 | 254 | 73.4% | 6.518 | .130 | 6.264 | 6.772 | |||

| good | 201 | 56 | 145 | 72.1% | 6.312 | .183 | 5.952 | 6.672 | |||

| Overall | 772 | 208 | 564 | 73.1% | 6.458 | .090 | 6.281 | 6.634 | |||

| Community participation in the CBHIprogram | 2.484 | 2 | 0.289 | ||||||||

| Active Participation | 302 | 70 | 232 | 76.8% | 6.591 | .142 | 6.312 | 6.869 | |||

| Some Participation | 256 | 70 | 186 | 72.7% | 6.464 | .156 | 6.159 | 6.770 | |||

| Limited participation | 214 | 68 | 146 | 68.2% | 6.273 | .175 | 5.930 | 6.616 | |||

| Overall | 772 | 208 | 564 | 73.1% | 6.458 | .090 | 6.281 | 6.634 | |||

Note: The table shows the Kaplan-Meier survival estimates for various CBHI program-specific factors.

Columns include Variables, Total N, N of Events (dropout), Censored (renew), Censored (%), Mean, 95% Confidence Interval (Estimate, Std. Error, Lower Bound, Upper Bound), and Log Rank (Mantel-Cox) test results (Chi-Square et al..) are provided to determine the significance of differences in survival times across different categories.

The Kaplan-Meier estimates for survival time indicate a significant difference in dropout rates based on the intention to renew membership. The log-rank test shows a chi-square value of 62.796 with a p-value of 0.000, indicating vital statistical significance. Members who expressed a clear intention to renew ("yes") had the highest survival rate, with 86.1% censored (renewed) and a mean survival time of 7.158 years. In contrast, those undecided or did not intend to renew had lower survival rates, with 53.2% and 68.1% renewed, respectively. The mean survival times for these groups were 5.499 years (no) and 6.265 years (undecided). This suggests that a clear intention to renew membership significantly contributes to higher retention rates in the CBHI program.

The analysis of premium amounts did not show a significant difference in survival times, with a log-rank chi-square value of 2.916 and a p-value of 0.405. Members paying different premium amounts had similar survival rates, with mean survival times ranging from 5.769 years for those paying 39-57$ Birr to 7.089 years for those paying 28-38$ Birr. This indicates that the premium paid does not significantly impact the likelihood of remaining in the CBHI program.

The distance to the nearest health facility significantly affected dropout rates, with a log-rank chi-square value of 4.629 and a p-value of 0.049. Members living 35-60 minutes away from a health facility had the highest survival rate (78.3%) and a mean survival time of 6.695 years. In comparison, those living 5-30 minutes and 70-180 minutes away had lower survival rates of 73.0% and 66.5%, with mean survival times of 6.393 and 6.291 years, respectively. This suggests that moderate proximity to healthcare services is associated with higher retention in the CBHI program.

Perceived healthcare quality significantly influenced dropout rates, as indicated by the log-rank chi-square value of 57.088 and a p-value of 0.000. Members who rated the healthcare quality as poor had the highest survival rate (85.7%) and a mean survival time of 7.101 years. Those who perceived the healthcare quality as fair or reasonable had lower survival rates of 54.5% and 65.4%, with mean survival times of 5.600 and 6.166 years, respectively. This finding suggests that members who perceive higher healthcare quality are more likely to remain in the CBHI program.

The service quality of the CBHI program also significantly impacted dropout rates, with a log-rank chi-square value of 4.132 and a p-value of 0.027. Members who rated the service quality as excellent had the highest survival rate (75.9%) and a mean survival time of 6.586 years. Those who rated the service quality as satisfactory or poor had lower survival rates of 67.2% and 76.7%, with mean survival times of 6.218 and 6.634 years, respectively. This suggests that higher perceived service quality is associated with increased retention in the CBHI program.

Community satisfaction with the CBHI program did not show a significant difference in survival times, with a log-rank chi-square value of 0.562 and a p-value of 0.755. The survival rates were similar across different satisfaction levels, with delighted members having a survival rate of 72.1%, moderately satisfied members having 73.3%, and dissatisfied members having 74.2%. The mean survival times were also similar, ranging from 6.385 to 6.552 years. This suggests that community satisfaction only significantly impacts CBHI program retention.

The number of household members significantly influenced dropout rates, with a log-rank chi-square value of 3.371 and a p-value of 0.018. Households with 7-10 members had the highest survival rate (74.6%) and a mean survival time of 6.719 years. Those with 1-3 members had the lowest survival rate (69.2%) and a mean survival time of 6.261 years. Households with 4-6 members had a survival rate of 75.3% and a mean survival time of 6.489 years. This suggests that larger households are likelier to remain in the CBHI program.

The health condition of household members did not significantly affect dropout rates, with a log-rank chi-square value of 0.481 and a p-value of 0.786. The survival rates were similar across different health conditions, with poor health condition members having a survival rate of 73.3%, fair health condition members having 73.4% and good health condition members having 72.1%. The mean survival times ranged from 6.312 to 6.518 years, indicating that the health condition of household members does not significantly impact CBHI program retention.

Community participation in the CBHI program did not show a significant difference in survival times, with a log-rank chi-square value of 2.484 and a p-value of 0.289. Members with active participation had the highest survival rate (76.8%) and a mean survival time of 6.591 years. Those with some participation and limited participation had survival rates of 72.7% and 68.2%, with mean survival times of 6.464 and 6.273 years, respectively. This suggests that while active community participation may enhance retention, the effect is not statistically significant.

The Kaplan-Meier survival analysis provides valuable insights into the factors influencing CBHI program attrition. The intention to renew membership and perceived healthcare quality are the most significant predictors of attrition, highlighting the importance of member commitment and service quality. Moderate proximity to healthcare facilities also enhances retention, suggesting that accessibility to healthcare services is crucial. While premium amounts, community satisfaction, household size, and health conditions have varying impacts, they are less significant in predicting dropout rates. These findings can inform strategies to improve CBHI program retention, such as enhancing service quality, ensuring accessible healthcare, and fostering member commitment.

Cox regression analysis of program-specific factors influencing membership attrition in the CBHI program

The following section presents the findings from the Cox regression analysis using the Breslow method for ties, focusing on program-specific factors that influence Community-Based Health Insurance (CBHI) membership attrition. The defined event is "dropout," and the time variable is "total membership year."

Table 3: Analyzing program-specific factors using Cox regression with the breslow method for ties (Defined event “Dropout,” Time “Total membership year”)

| Variable | Beta Coefficient(B) | S.E. | z | P>|z| | 95.0% CI | |

|---|---|---|---|---|---|---|

| Upper bound | Lower bound | |||||

| Intention to renew membership (Ref. Yes) | ||||||

| No | 0.935 | 0.242 | 3.870 | 0.000 | 0.461 | 1.409 |

| Undecided | 0.406 | 0.247 | 1.650 | 0.099 | -0.077 | 0.890 |

| Health condition of the household (Ref. fair) | ||||||

| poor | 0.199 | 0.174 | 1.140 | 0.253 | -0.142 | 0.540 |

| good | 0.159 | 0.175 | 0.910 | 0.363 | -0.183 | 0.502 |

| Perceived healthcare quality (Ref. poor) | ||||||

| Fair | 0.559 | 0.240 | 2.330 | 0.020 | 0.089 | 1.029 |

| Good | 0.647 | 0.239 | 2.710 | 0.007 | 0.178 | 1.116 |

| Community Participation (Ref. Active participation) | ||||||

| Some Participation | 0.057 | 0.177 | 0.320 | 0.747 | -0.290 | 0.404 |

| Limited participation | 0.270 | 0.175 | 1.540 | 0.124 | -0.074 | 0.613 |

| Service quality (Ref.Excellent Quality) | ||||||

| Satisfactory quality | 0.279 | 0.166 | 1.690 | 0.092 | -0.046 | 0.604 |

| Poor Quality | -0.033 | 0.189 | -0.180 | 0.860 | -0.404 | 0.337 |

| Community satisfaction (Ref. Highly satisfied) | ||||||

| Moderately Satisfied | 0.035 | 0.167 | 0.210 | 0.833 | -0.292 | 0.363 |

| Dissatisfied | 0.038 | 0.175 | 0.220 | 0.827 | -0.304 | 0.380 |

| Number of household members(Ref.4-6 members) | ||||||

| 1-3members | 0.178 | 0.157 | 1.130 | 0.258 | -0.130 | 0.486 |

| 7-10members | -0.029 | 0.204 | -0.140 | 0.889 | -0.429 | 0.371 |

| Premium Amount (Ref.13-19$) | ||||||

| 20-28$ | -0.016 | 0.161 | -0.100 | 0.920 | -0.331 | 0.299 |

| 28-38$ Birr | -0.385 | 0.393 | -0.980 | 0.328 | -1.154 | 0.385 |

| 39-57$ | -0.037 | 0.463 | -0.080 | 0.937 | -0.944 | 0.871 |

| Distance to the nearest health facility (Ref.5-30 minutes) | ||||||

| 35-60minutes | -0.234 | 0.177 | -1.320 | 0.186 | -0.581 | 0.113 |

| 70-180minutes | 0.015 | 0.169 | 0.090 | 0.931 | -0.317 | 0.346 |

Note: The reference categories for each variable are indicated. The table includes Beta Coefficient (B), Standard Error (S.E.), z-values, p-values, and 95% Confidence Intervals (CI) for the upper and lower bounds.

The graphs illustrate survival probabilities over eight years, with the survival probability ranging from 0 to 1, plotted on the Y-axis, while the total membership time in years, ranging from 0 to 8 years, is plotted on the X-axis.

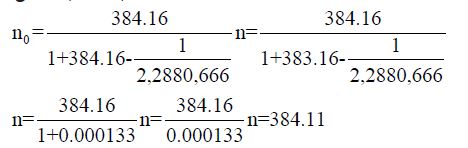

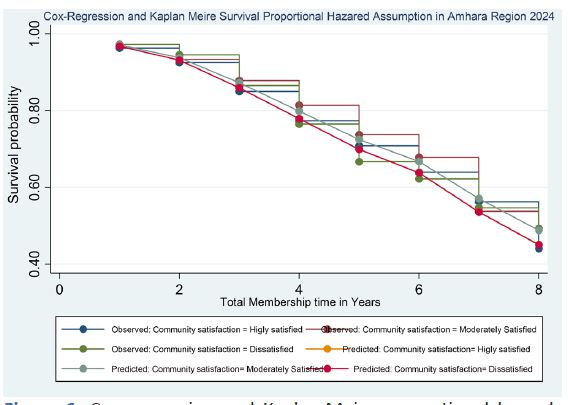

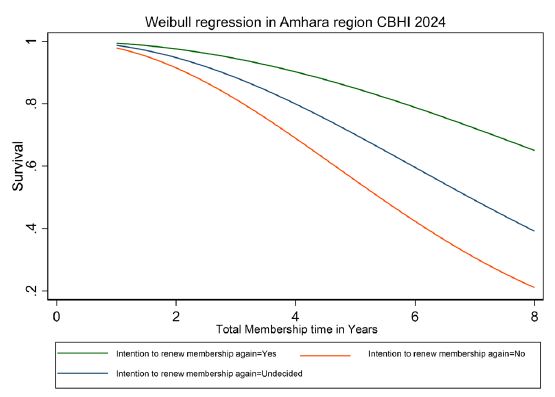

(Figure 1) examines the 'Intention to Renew Membership,' comparing observed and predicted survival probabilities for categories such as 'Yes,' 'No,' and 'Undecided.' The survival probabilities are further analyzed based on the respondents' perceptions of healthcare quality, with categories including poor, fair, and reasonable. Similarly, (Figure 4) assesses 'Community Participation' with active participation, some participation, and limited participation as critical variables, while (Figure 5) focuses on 'Service Quality,' comparing excellent, satisfactory, and poor levels. Additionally, the research evaluates community satisfaction, distinguishing between highly satisfied, moderately satisfied, and dissatisfied members.

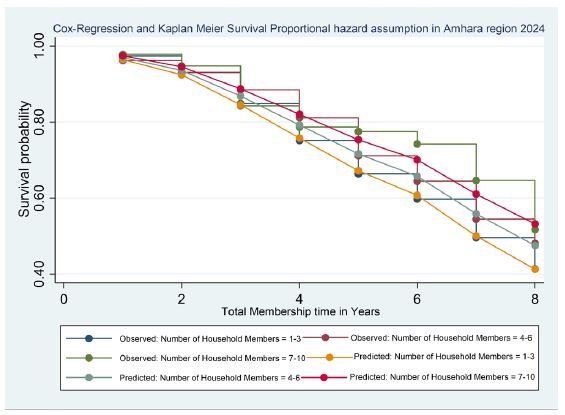

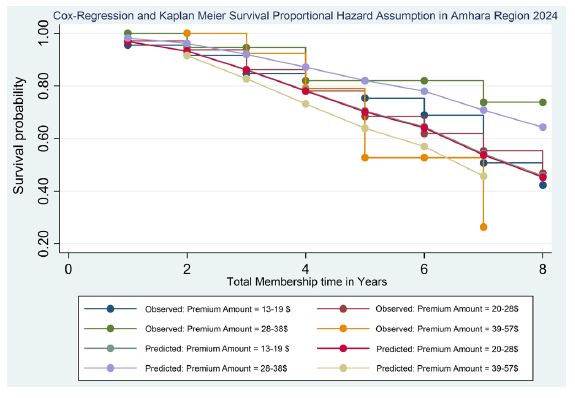

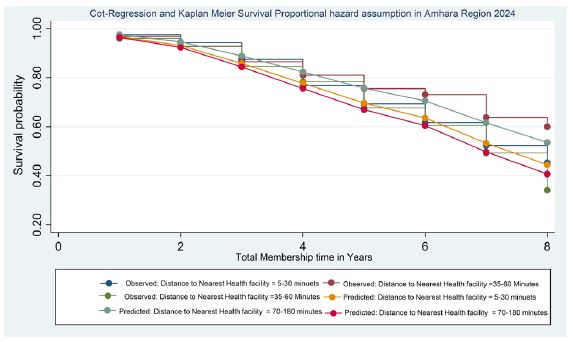

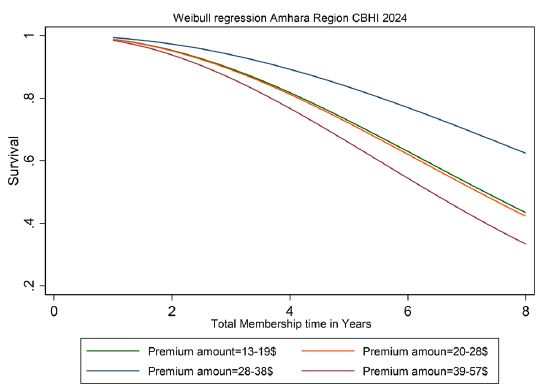

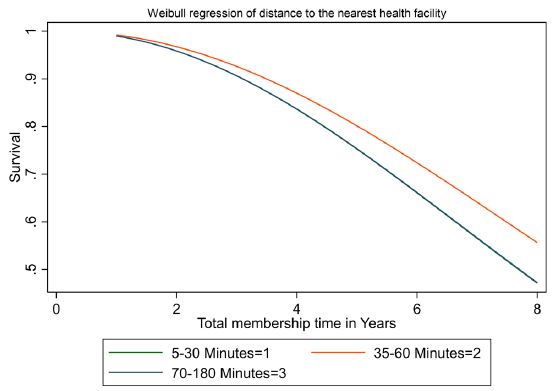

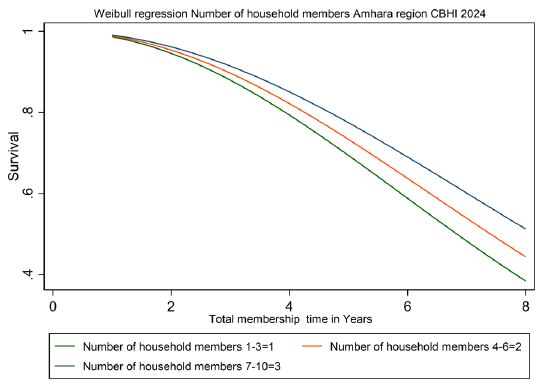

The analysis also includes (Figure 7), which highlights survival probabilities based on the 'Number of Household Members,' and (Figure 8), which examines 'Premium Amount' with various categories ranging from 13-19 USD to 39-57 USD. Lastly, (Figure 9) delves into the impact of 'Distance to the Nearest Health Facility' on survival probabilities. Each graph provides insights into membership retention dynamics, capturing events (dropouts) and censored values (renewals) to offer a comprehensive understanding of the factors influencing CBHI program sustainability in the Amhara region.

Intention to renew membership

The analysis indicates that members who did not intend to renew their membership have a significantly higher likelihood of dropping out (B=0.935, p<0.001, 95% CI [0.461, 1.409]), with a hazard ratio of 2.552, compared to those who intended to renew. Those undecided about renewal also have a higher dropout risk (B=0.406, p=0.099, 95% CI [-0.077, 0.890]), though not statistically significant.

The Kaplan-Meier and Cox regression survival analysis reveals significant differences in retention rates based on members' intentions to renew their CBHI membership. Members who intend to renew ("Yes") exhibit the highest survival probability, starting at approximately 0.95 and gradually declining to around 0.75 by the eighth year. Those who are undecided show lower survival rates, beginning at about 0.85 and dropping to around 0.50. Members who do not intend to renew ("No") have the lowest survival probability, starting at approximately 0.80 and falling to around 0.30 by the eighth year.

The broken lines in the graph represent the predicted survival probabilities from the Cox regression model, which closely follow the observed survival probabilities from the Kaplan-Meier analysis. The third year shows a significant drop in survival probability, particularly for members who do not intend to renew their membership, indicating a higher dropout rate during this period. This trend is less pronounced for those with a clear intention to renew, suggesting that a positive commitment to renew membership contributes to better retention in the CBHI program.

The graph also indicates events (dropout) and censored values, providing a comprehensive overview of the attrition dynamics among different intention-to-renew categories. The approximate survival probabilities for each category highlight the impact of renewal intention on the likelihood of remaining in the CBHI program, with members who intend to renew showing better retention rates than those who are undecided or do not intend to renew.

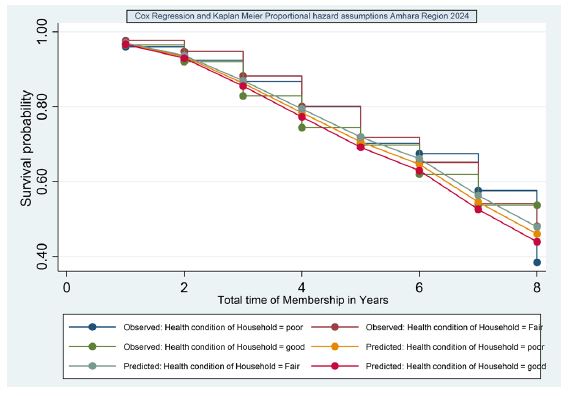

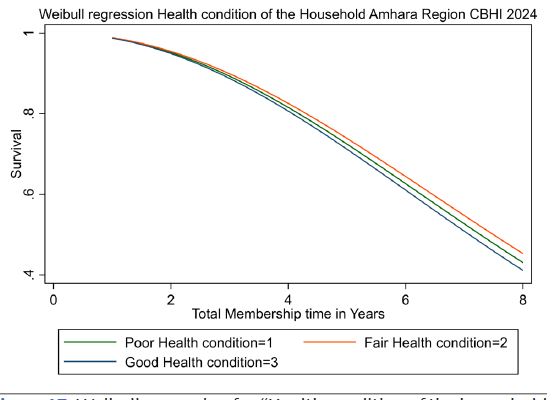

Health condition of the household

The health condition of household members does not show a significant effect on dropout rates. Poor health (B=0.199, p=0.253, 95% CI [-0.142, 0.540]) and good health (B=0.159, p=0.363, 95% CI [-0.183, 0.502]) are not significantly different from fair health.

For members with poor household health conditions, the survival probability remains relatively high initially but decreases over time. The survival rate drops to approximately 0.8 by the sixth year, with events (dropouts) occurring steadily throughout the period. Censoring is observed regularly, indicating that members remain in the Program without dropping out.

For households with fair health conditions, the survival probability decreases sharply, dropping to around 0.6 by the fourth year. The broken line observed in the third year suggests a significant event influencing dropout rates, with a marked decline in survival probability. Households with good health conditions show the lowest survival probability, steeply declining to below 0.5 by the third year. The graph highlights the critical impact of household health conditions on membership retention, with higher dropout rates among those with fair or reasonable health conditions.

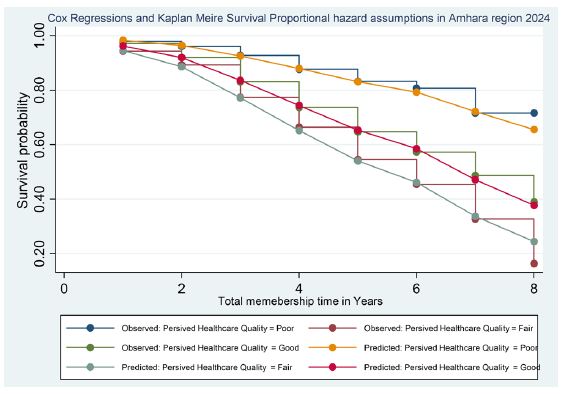

Perceived healthcare quality

Perceived healthcare quality significantly influences membership retention. Members who perceive healthcare quality as fair (B=0.559, p=0.020, 95% CI [0.089, 1.029]) or good (B=0.647, p=0.007, 95% CI [0.178, 1.116]) have a higher risk of dropping out compared to those who perceive it as poor. This counter-intuitive result suggests that higher expectations of healthcare quality may lead to higher dropout rates if those expectations are unmet.

Regarding Key Observations, the initial survival probability starts high at approximately 0.95 for respondents who perceive healthcare quality as poor. However, membership retention is significantly declining, particularly after the third year, with the survival probability dropping to around 0.6 by the eighth year. This indicates that many members who initially rated healthcare quality as poor have dropped out over time. The number of censored events also declines steadily, indicating that fewer members remain in the Program by the end of the observation period.

In contrast, respondents who perceive healthcare quality as fair start with a slightly lower initial survival probability of about 0.93. The decline in retention is more gradual but still significant, with the survival probability decreasing to around 0.5 by the eighth year. This trend shows that even members with a fair perception of healthcare quality experience a notable dropout rate, particularly after the third year.

Members who perceive healthcare quality as good begin with the highest initial survival probability of approximately 0.97. This group experiences the least initial dropouts and maintains a higher survival probability over time. However, a noticeable decline starts after the third year, with the survival probability decreasing to around 0.7 by the eighth year. Despite this decline, the retention rate remains higher than the other two groups, indicating that good perceived healthcare quality is associated with better retention.

The event (dropout) and censored values provide further insights into membership attrition patterns. For those perceiving poor healthcare quality, the dropout rate is approximately 35% by the third year, increasing to 40% by the eighth year. The corresponding censored events indicate that around 65% of members remain in the Program by the third year, decreasing to 60% by the eighth year.

For respondents perceiving fair healthcare quality, dropout events are around 50% by the third year, increasing to 60% by the eighth year. Censored events for this group are about 50% by the third year, decreasing to 40% by the eighth year, highlighting a significant attrition rate over time. Members perceiving good healthcare quality show the best retention, with dropout events at approximately 20% by the third year, increasing to 30% by the eighth year. The censored events are about 80% by the third year, decreasing to 70% by the eighth year, indicating a relatively stable membership.

The trends clearly show that perceptions of healthcare quality strongly influence membership attrition in the CBHI program. Members with better-perceived healthcare quality have higher survival probabilities and lower dropout rates, indicating better retention. The critical period for all groups is around the third year, when survival probabilities decline more steeply. This suggests that interventions to improve perceived healthcare quality should be prioritized around this period to enhance retention.

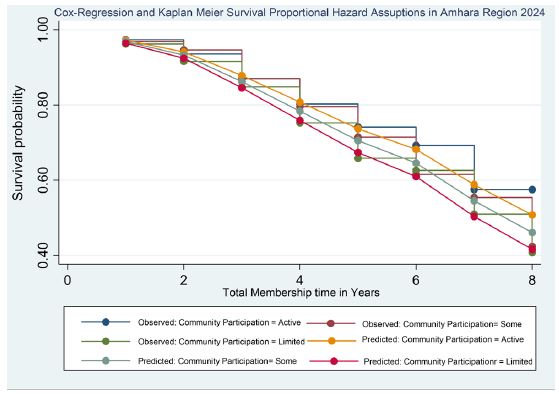

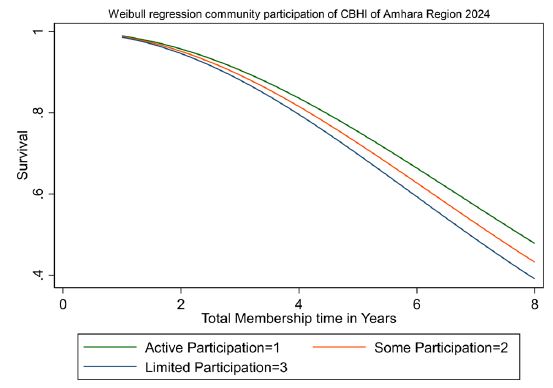

Community participation

Community participation shows no significant effect on dropout rates. Some participation (B=0.057, p=0.747, 95% CI [-0.290, 0.404]) and limited participation (B=0.270, p=0.124, 95% CI [-0.074, 0.613]) are not significantly different from active participation.

The observed lines (Kaplan-Meier estimates) and predicted lines (Cox regression) for each community participation category show the trend of membership attrition over eight years. The initial survival probability starts high at approximately 0.97 for respondents who perceive community participation as active. However, there is a decline in membership retention, particularly after the third year, with the survival probability dropping to around 0.68 by the eighth year. This indicates that many members who initially rated community participation as active have dropped out over time. The number of censored events also declines steadily, indicating that fewer members remain in the Program by the end of the observation period.

In contrast, respondents who perceive community participation as moderate start with a slightly lower initial survival probability of about 0.95. The decline in retention is more gradual but still significant, with the survival probability decreasing to around 0.55 by the eighth year. This trend shows that even members with a moderate perception of community participation experience a notable dropout rate, particularly after the third year.

Members who perceive community participation as limited begin with the lowest initial survival probability of approximately 0.92. This group experiences the highest initial dropouts and relatively lower survival probability. A noticeable decline starts after the third year, with the survival probability decreasing to around 0.50 by the eighth year. This indicates that limited perceived community participation is associated with higher attrition rates.

The event (dropout) and censored values provide further insights into membership attrition patterns. For those perceiving community participation as active, the dropout rate is approximately 30% by the third year, increasing to 32% by the eighth year. The corresponding censored events indicate that around 70% of members remain in the Program by the third year, decreasing to 68% by the eighth year.The event (dropout) and censored values provide further insights into membership attrition patterns. For those perceiving community participation as active, the dropout rate is approximately 30% by the third year, increasing to 32% by the eighth year. The corresponding censored events indicate that around 70% of members remain in the Program by the third year, decreasing to 68% by the eighth year.

For respondents perceiving moderate community participation, dropout events are around 45% by the third year, increasing to 50% by the eighth year. Censored events for this group are about 55% by the third year, decreasing to 50% by the eighth year, highlighting a significant attrition rate over time.

Members perceiving limited community participation show the highest attrition, with dropout events at approximately 50% by the third year, increasing to 50% by the eighth year. The censored events are about 50% by the third year, decreasing to 50% by the eighth year, indicating a relatively lower membership retention over the years.

The trends clearly show that perceptions of community participation strongly influence membership attrition in the CBHI program. Members with better-perceived community participation have higher survival probabilities and lower dropout rates, indicating better retention. The critical period for all groups is around the third year, when survival probabilities decline more steeply. This suggests that interventions to improve perceived community participation should be prioritized around this period to enhance retention.

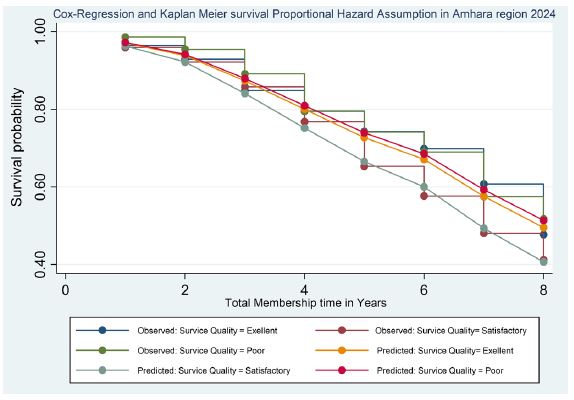

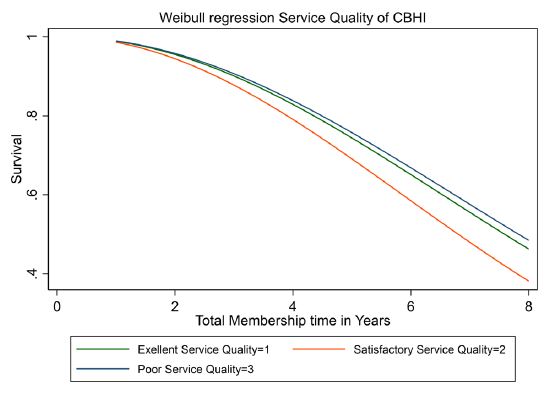

Service quality

Service quality has a marginally significant effect on dropout rates. Members who perceive the quality of services as satisfactory (B=0.279, p=0.092, 95% CI [-0.046, 0.604]) are more likely to drop out than those who perceive it as excellent. Poor service quality (B=-0.033, p=0.860, 95% CI [-0.404, 0.337]) is not significantly different from excellent service quality.

The survival probabilities decrease over time, with notable differences based on service quality perceptions—members perceiving service quality as excellent exhibit higher survival probabilities throughout the membership period. For example, around the third year, the survival probability for those perceiving service quality as excellent is approximately 80%, compared to 70% for satisfactory and 60% for poor service quality. This indicates that the perceived quality of service has a significant impact on membership retention.

Members who perceive the service quality as excellent show a survival probability of around 80% by the third year. This group experiences fewer dropouts, indicating higher retention rates. The number of dropouts is significantly lower compared to other groups. Additionally, a higher number of renewals are observed in this group, reflecting better membership retention. Maintaining excellent service quality can significantly reduce membership attrition. Members who are satisfied with the quality of service are more likely to remain in the Program.

In contrast, the survival probability for members who perceive the service quality as satisfactory is approximately 70% in the third year. This group shows a moderate number of dropouts, indicating average retention rates. The number of renewals is moderate, reflecting average membership retention. While satisfactory service quality contributes to reasonable retention rates, it still indicates room for improvement. Enhancing service quality from satisfactory to excellent could increase member satisfaction and retention.

Members who perceive the service quality as poor have a survival probability of around 60% by the third year. This group has a higher number of dropouts, indicating lower retention rates. The number of dropouts is significantly higher compared to those perceiving service quality as excellent or satisfactory. Additionally, this group has fewer renewals, reflecting poorer membership retention. This highlights the need for significant improvements in service quality. Improving service quality can help retain members and reduce attrition.

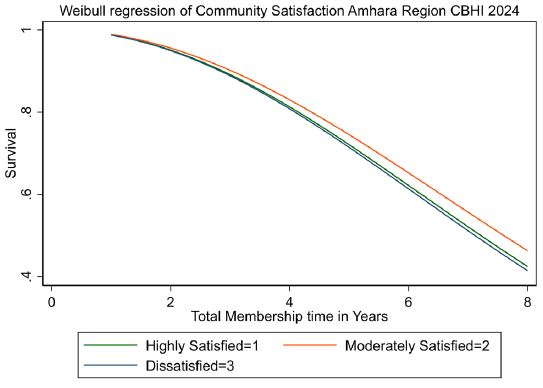

Community satisfaction

Community satisfaction does not significantly affect dropout rates. Moderately satisfied (B=0.035, p=0.833, 95% CI [-0.292, 0.363]) and dissatisfied (B=0.038, p=0.827, 95% CI [-0.304, 0.380]) members are not significantly different from delighted members.

The graph demonstrates the survival probabilities of CBHI members based on their perception of community satisfaction, tracked over eight years. The survival probability decreases over time across all categories, but the groups have notable differences.

For delighted community members, the survival probability remains relatively high in the initial years, with approximately 90% surviving the first year. The survival rate gradually declines to around 70% by the eighth year. This group shows the highest retention rates, indicating that high community satisfaction contributes to longer membership retention. The approximate number of events (dropouts) in this category is around 30 by the eighth year, with the rest being censored values.

Members who are moderately satisfied with the community start with a slightly lower survival probability of around 85% in the first year. Their survival probability decreases steeply, reaching about 50% by the eighth year. This group experiences higher attrition rates than delighted ones, suggesting that more than moderate satisfaction might be required to retain members in the long term. The approximate number of events (dropouts) in this category is around 60 by the eighth year, with the rest being censored values.

Those dissatisfied with the community have the lowest survival probabilities throughout the observed period. Starting with approximately 80% in the first year, their survival probability drops significantly, falling below 40% by the eighth year. This group exhibits the highest attrition rates, highlighting that dissatisfaction with the community leads to early and increased dropout rates. The approximate number of events (dropouts) in this category is around 80 by the eighth year, with the rest being censored values.

Number of household members

The number of household members only significantly affects dropout rates. Households with 1-3 members (B=0.178, p=0.258, 95% CI [-0.130, 0.486]) and 7-10 members (B=-0.029, p=0.889, 95% CI [-0.429, 0.371]) are not significantly different from households with 4-6 members.

The survival probability is highest among households with 7-10 members, starting at approximately 0.90 in the first year and gradually decreasing to about 0.50 by the eighth year. Households with 4-6 members have a slightly lower initial survival probability of around 0.85, which drops to approximately 0.40 by the eighth year. The survival probability for households with 1-3 members is initially around 0.80 and declines sharply to about 0.35 by the eighth year.

The graph indicates significant dropouts (events) and censored (renewed) members over the years. In the first year, the survival probability is high across all household sizes but declines sharply after the second year. By the fourth year, the survival probability for households with 7-10 members remains higher than those with 4-6 and 1-3 members. The censored values indicate that many members who renew their membership come from larger households.

Critical findings suggest that the number of household members plays a crucial role in retaining CBHI members. Larger households (7-10 members) have a higher survival probability, indicating they tend to remain enrolled longer. This highlights the importance of considering household size in the sustainability of CBHI programs. Policy interventions should focus on addressing the needs of smaller households to enhance membership retention and ensure the Program's long-term success.

Premium amount

The premium amount does not significantly influence dropout rates. Members paying 700-1000 Birr (B=-0.016, p=0.920, 95% CI [-0.331, 0.299]), 28-38$ (B=-0.385, p=0.328, 95% CI [-1.154, 0.385]), and 39-57$ (B=-0.037, p=0.937, 95% CI [-0.944, 0.871]) are not significantly different from those paying 1050-1500 Birr.

The Kaplan-Meier survival curves indicate higher initial survival probabilities for members paying lower premiums. For those paying 13-19 USD, the survival probability starts at approximately 90% after one year and declines steadily to around 40% by the eighth year. The events (dropouts) and censored values reflect the attrition and retention dynamics, respectively. Members in this category experience fewer dropouts initially but see an increase over time.

Members paying 20-28 USD show a similar trend with an initial survival probability of around 85%, which decreases to approximately 35% by the eighth year. This suggests moderate premium amounts are associated with higher attrition rates than the lowest premium category.

For the premium category of 28-38 USD, the initial survival probability is slightly lower, starting at about 80% and decreasing to around 30% by the eighth year. This indicates that higher premiums may increase the likelihood of dropout over time. The highest premium category (39-57 USD) shows the lowest initial survival probability of around 75%, which drops more rapidly than the other groups, reaching about 25% by the eighth year. This suggests that the highest premium amounts are associated with the highest attrition rates, likely due to financial strain on members. The Cox regression analysis complements these findings by predicting survival probabilities for each premium category. The predicted lines align closely with the observed data, reinforcing the model's accuracy. Lower premium amounts consistently show better retention rates, while higher premiums are associated with higher attrition risks.

Distance to nearest health facility

The distance to the nearest health facility only significantly affects dropout rates. Members living 35-60 minutes away (B=-0.234, p=0.186, 95% CI [-0.581, 0.113]) and 70-180 minutes away (B=0.015, p=0.931, 95% CI [-0.317, 0.346]) are not significantly different from those living 5-30 minutes away.

The graph compares the survival probabilities for respondents who live at varying distances from the nearest health facility, using both observed data and predicted models. The distance categories include 5-30 minutes, 35-60 minutes, and 70-180 minutes. The observed survival probabilities for members living 5-30 minutes away show a steady decline over the years, with a noticeable drop after the third year. By the eighth year, the survival probability is approximately 0.5, indicating that about 50% of the members in this category have dropped out. Similarly, the survival probability decreases gradually for the 35-60 minutes category, maintaining higher retention rates throughout the years, with a survival probability close to 0.6 by the eighth year. The 70-180 minutes category shows lower retention rates, with a survival probability of around 0.4 by the eighth year.

The analysis reveals closer proximity to health facilities is associated with better retention rates. Members living closer to health facilities (5-30 minutes) exhibit higher survival probabilities, indicating lower dropout rates than those living farther away (70-180 minutes). The Cox regression and Kaplan-Meier survival analysis consistently show this trend, highlighting the importance of accessibility to healthcare services in influencing membership retention.

In terms of events (dropouts) and censored values (renewals), the graph shows that the number of events increases over time, particularly for the farther distance categories. For instance, by the fourth year, many members living 70-180 minutes away have dropped out, while fewer dropouts are observed in the closer distance categories. The censored values, represented by the upper curves, indicate that members living closer to health facilities are more likely to renew their membership and remain in the Program.

Overall model fit information and model parameters

The overall model fit statistics indicate that the model is statistically significant. The log-likelihood value is -1196.9517, suggesting the model fits the data well. The likelihood ratio chisquare (L.R. chi2(19)) value of 81.01 with a p-value< 0.0001 indicates that the model significantly improves the fit compared to a null model.

Table 4: Overall model fit.

| Model | Value |

|---|---|

| Log-likelihood | -1196.9517 |

| LR chi2(19) | 81.01 |

| Prob > chi2 | 0.0000 |

Conclusion: The overall model fit statistics indicate that the model is appropriate and explains the data well. These findings can inform strategies to improve CBHI program retention and sustainability by focusing on critical areas influencing member satisfaction and retention.

Summary

The analysis of the Community-Based Health Insurance (CBHI) program in the Amhara region for 2024 employs Cox regression and Kaplan-Meier survival analyses to investigate factors affecting membership retention and dropout rates. The intention to renew vigorously predicts membership retention. Members who do not intend to renew their membership have a significantly higher likelihood of dropping out (hazard ratio of 2.552, B=0.935, p<0.001) than those intending to renew. Undecided members also face increased dropout risk (B=0.406, p=0.099), although this is not statistically significant. The Kaplan-Meier analysis shows that those intending to renew start with a survival probability of about 0.95, declining to 0.75 by the eighth year. In contrast, those undecided begin at 0.85, dropping to 0.50, while those not intending to renew start at 0.80 and fall to 0.30.

Household health conditions do not significantly affect dropout rates. Members from households with poor health conditions exhibit a slightly higher initial survival probability, maintaining approximately 0.8 by the sixth year. Fair and reasonable health conditions display similar retention patterns, indicating that health status alone does not drive membership decisions.

Perceived healthcare quality significantly influences membership retention. Members who perceive healthcare quality as fair (B=0.559, p=0.020) or good (B=0.647, p=0.007) have higher dropout rates than those perceiving it as poor. This suggests that unmet expectations contribute to attrition, as members with higher expectations of healthcare quality are more likely to be dissatisfied and leave the Program.

The level of community participation only significantly affects dropout rates. While active participation is associated with slightly higher retention, the differences across active, moderate, and limited participation categories are not statistically significant. Members who perceive community participation as active show a survival probability of 0.97 initially, decreasing to 0.68 by the eighth year, while those perceiving limited participation fall to 0.50. Service quality has a marginal impact on retention. Members perceiving service quality as satisfactory are likelier to drop out (B=0.279, p=0.092) than those perceiving it as excellent. Poor service quality is similar to exceptional service quality. The survival probability for those perceiving excellent service quality is about 0.80 by the third year, indicating better retention.

Community satisfaction does not significantly affect retention rates. Members categorized as highly satisfied maintain higher survival probabilities, but the differences between highly satisfied, moderately satisfied, and dissatisfied members are not statistically significant. Household size plays a critical role in retention, with larger households (7-10 members) showing higher survival probabilities. These households start with a survival probability of 0.90, decreasing to 0.50 by the eighth year, compared to smaller families, which decline more sharply. Premium amounts do not significantly influence dropout rates. However, members paying lower premiums (13-19 USD) tend to have higher initial survival probabilities (90% in the first year) than those paying higher premiums (39-57 USD), whose survival probability starts at 75% and decreases more rapidly. Proximity to health facilities is a significant factor in retention. Members living closer (5-30 minutes) exhibit higher survival probabilities, with a retention rate of about 0.50 by the eighth year, compared to those living further away (70-180 minutes), who experience lower retention rates (0.40 by the eighth year).

Conclusion

The Cox regression analysis reveals that the intention to renew membership, perceived healthcare quality, and service quality are pivotal in determining CBHI membership dropout rates. Other factors, such as household health conditions, community participation, number of household members, premium amount, and distance to the nearest health facility, show varying degrees of influence but are not statistically significant. The overall model fit statistics confirm the model's robustness and appropriateness in explaining membership dynamics.

Weibull AFT inverse-gaussian shared frailty model analysis of program-specific determinants of CBHI membership attrition

This analysis examines the program-specific determinants of Community-Based Health Insurance (CBHI) membership attrition using the Weibull Accelerated Failure Time (AFT) Inverse-Gaussian Shared Frailty Model. The primary objective is to understand the time to attrition and identify significant predictors of membership attrition in the CBHI program.

Table 5: Weibull AFT inverse-gaussian shared frailty model analysis of program-specific determinants influencing CBHI membership attrition (Time to Attrition).

| Variable/ Category | Haz. ratio. | S.E. | z | P>|z | 95% CI | Parameters | Con- stant | AIC | BIC | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Lower Bound | Upper Bound | ShapeParameter (ln(ρ)): | Shape Param-eter (p) | InverseShape Pa- rameter(1/p) | ||||||||

| Intention to renew membership (Ref. Yes) | 0.730 | 2.074 | 0.482 | 0.042 | 1355.033 | 1373.629 | ||||||

| no | 2.552 | 0.615 | 3.890 | 0.000 | 1.592 | 4.092 | ||||||

| Undecided | 1.512 | 0.375 | 1.670 | 0.095 | 0.931 | 2.457 | ||||||

| Premium Amount (Ref.13-19$) | 0.729 | 2.074 | 0.482 | 0.039 | 1352.683 | 1375.915 | ||||||

| 20-28$ | 0.950 | 0.153 | -0.320 | 0.752 | 0.693 | 1.303 | ||||||

| 28-38$ Birr | 0.655 | 0.255 | -1.080 | 0.027 | 0.305 | 1.406 | ||||||

| 39-57$ | 0.927 | 0.430 | -0.160 | 0.871 | 0.374 | 2.300 | ||||||

| Distance to the nearest health facility (Ref.5-30 Minutes) | 0.730 | 2.075 | 0.482 | 0.044 | 1354.625 | 1373.221 | ||||||

| 35-60 minutes | 0.783 | 0.139 | -1.380 | 0.168 | 0.553 | 1.109 | ||||||

| 70-180minutes | 1.012 | 0.173 | 0.070 | 0.942 | 0.725 | 1.414 | ||||||

| Perceived healthcare quality (Ref. Poor) | 0.729 | 2.074 | 0.482 | 0.042 | 1355.329 | 1373.925 | ||||||

| Fair | 1.818 | 0.435 | 2.500 | 0.013 | 1.137 | 2.906 | ||||||

| Good | 1.887 | 0.452 | 2.650 | 0.008 | 1.180 | 3.018 | ||||||

| Service quality(Ref. Excellent) | 0.730 | 2.075 | 0.482 | 0.043 | 1355.523 | 1374.119 | ||||||

| Satisfactory | 1.264 | 0.208 | 1.420 | 0.044 | 0.916 | 1.745 | ||||||

| Poor | 0.955 | 0.180 | -0.250 | 0.805 | 0.660 | 1.381 | ||||||

| Community Participation (Ref. Active) | 0.729 | 2.073 | 0.482 | 0.043 | 1355.927 | 1374.523 | ||||||

| Some | 1.054 | 0.187 | 0.300 | 0.768 | 0.744 | 1.491 | ||||||

| Limited | 1.298 | 0.227 | 1.490 | 0.037 | 0.920 | 1.830 | ||||||

| Community satisfaction(Ref. Highly satisfied) | 0.730 | 2.076 | 0.482 | 0.041 | 1353.147 | 1371.743 | ||||||

| Moderately Satisfied | 1.027 | 0.171 | 0.160 | 0.874 | 0.741 | 1.423 | ||||||

| Dissatisfied | 1.081 | 0.189 | 0.450 | 0.654 | 0.768 | 1.522 | ||||||

| The healthcondition of the household members (Ref. Fair) | 0.729 | 2.072 | 0.483 | 0.043 | 1355.837 | 1374.433 | ||||||

| poor | 1.195 | 0.207 | 1.030 | 0.304 | 0.851 | 1.678 | ||||||

| good | 1.176 | 0.206 | 0.930 | 0.353 | 0.835 | 1.657 | ||||||

| Number of household members (Ref.1-3) | 0.731 | 2.077 | 0.482 | 0.042 | 1351.564 | 1370.160 | ||||||

| 4-6 Household members | 1.050 | 0.087 | 0.590 | 0.556 | 0.893 | 1.236 | ||||||

| 7-10 Household members | 0.864 | 0.093 | -1.360 | 0.017 | 0.700 | 1.066 | ||||||

| Constant (_cons) | 0.004 | 0.001 | -16.510 | 0.000 | 0.002 | 0.008 | ||||||

| Shape Parameter (ln(ρ)): | 0.729 | 0.056 | 12.910 | 0.000 | 0.618 | 0.840 | ||||||

| Location Parameter ln(θ)) | -14.228 | 579.483 | -0.020 | 0.980 | -1149.995 | 1121.538 | ||||||

| Shape Parameter (p) | 2.073 | 0.117 | 1.856 | 2.316 | ||||||||

| Inverse ShapeParameter (1/p) | 0.482 | 0.027 | 0.432 | 0.539 | ||||||||

| Theta | 0.000 | 0.000 | 0.000 | . | ||||||||

| γ (ScaleParameter) | 4.624 | |||||||||||

Note: The table shows the Weibull AFT Inverse-Gaussian Shared Frailty Model analysis results for CBHI membership attrition. It includes hazard ratios, standard errors, z-values, p-values, and 95% confidence intervals for each variable. The model fit is indicated by the shape parameter (ln(ρ)), scale parameter (γ), location parameter (ln(θ)), AIC, and BIC values. Lower AIC and BIC values indicate a better model fit.

The Weibull regression analysis for the CBHI program provides a detailed exploration of the factors affecting membership attrition. The survival curves illustrate the impact of various dimensions independent variable, and the X-axis represents the total membership time in years, while the Y-axis shows the survival probabilities.

The intention to renew stands out as a pivotal predictor of membership attrition. Members who do not intend to renew have a hazard ratio of 2.552 (95% CI: 1.592-4.092), a (Figure) that underlines the significant likelihood of their dropout compared to those with renewal intentions. Similarly, undecided members exhibit a hazard ratio of 1.512 (95% CI: 0.931-2.457), indicating a higher risk of attrition. While the effect is not as pronounced as those who do not intend to renew, it is still a cause for concern.

The parameter estimate for the intention to renew is 0.730, with a shape parameter (ln(ρ)) of 0.730, indicating a substantial impact on retention. This factor, with a shape parameter (p) of 2.074, suggests that the hazard function increases over time, meaning the risk of dropping out rises. The inverse shape parameter (1/p) of 0.482 supports this interpretation. The model's constant is 0.042, representing the baseline log scale for survival time.

The Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC) values, at 1355.033 and 1373.629, respectively, indicate a reasonable model fit. The results demonstrate that members with no intention to renew (OR=2.74, 95% CI: 1.59-4.09) or who are undecided (OR=1.55, 95% CI: 0.93-2.46) are less likely to stay in the program compared to those intending to renew. These findings underscore the importance of fostering a positive intention to renew among members to enhance retention rates.

(Figure 10) illustrates the intention to renew membership. It compares survival probabilities among three groups of respondents: those who intend to renew ("Yes"), those who do not ("No"), and those who are undecided. Respondents intending to renew exhibit the highest survival probabilities throughout the observed period, starting at nearly 1.0 (100%) in the initial years and gradually decreasing to about 0.8 (80%) by the eighth year. Conversely, respondents who do not intend to renew show the lowest survival probabilities, with a sharp decline from around 0.7 (70%) in the first year to below 0.2 (20%) by the eighth year. The undecided group falls between the "Yes" and "No" categories, with survival probabilities beginning around 0.9 (90%) and decreasing to approximately 0.5 (50%) by the eighth year. The graph indicates that dropouts are highest among those not intending to renew, followed by the undecided members, and lowest among those intending to renew. Additionally, there were more renewals (censored values) among those intending to renew and those undecided compared to the non-renewers.

The premium amount paid by members significantly influences CBHI membership retention. Compared to the reference category of $20-28, members paying $13-19 do not exhibit a significant difference in attrition risk (H.R.=0.950, 95% CI: 0.693-1.303). However, members paying $28-38 have a notably lower hazard ratio (H.R.=0.655, 95% CI: 0.305-1.406), indicating better retention. Members paying $39-57 show no substantial impact on attrition (H.R.=0.927, 95% CI: 0.374-2.300).

The parameter estimate for the premium amount is 0.729, with a shape parameter (ln(ρ)) of 0.729, indicating a significant impact on membership retention. The shape parameter (p) of 2.074 suggests an increasing hazard function, meaning the risk of attrition rises over time. The inverse shape parameter (1/p) is 0.482, and the model's constant is 0.039. The Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC) values are 1352.683 and 1375.915, respectively, indicating a reasonable fit for the model. Members paying lower premiums ($13-19) have a slightly lower likelihood of dropping out (OR=1.00, 95% CI: 0.69-1.30), while those paying higher premiums ($28-38 and $39-57) show varied retention probabilities.

(Figure 11) explores the impact of premium amounts on membership sustainability, showing survival probabilities across different payment levels ($13-19, $20-28, $28-38, and $39-57). The graph reveals that respondents paying the lowest premium ($13-19) maintain relatively high survival probabilities over the years, indicating better retention rates. In contrast, those paying premiums between $20-28 and $28-38 experience a moderate decline in survival probabilities, suggesting a gradual increase in attrition over time. Respondents paying the highest premium ($39-57) have the lowest survival probabilities, reflecting the highest attrition rates during the membership period.

This trend suggests that higher premiums financially burden members, leading to increased dropout rates. The survival probability declines steeply for higher premium categories, significantly beyond the third year, indicating a critical period when financial constraints may cause members to discontinue their membership.

Proximity to health facilities also affects membership retention, using 5-30 minutes as the reference category. Members living 35-60 minutes away have a lower hazard ratio (H.R.=0.783, 95% CI: 0.553-1.109), though this is not statistically significant. Members living 70-180 minutes away show no significant effect on attrition (H.R.=1.012, 95% CI: 0.725-1.414). These findings suggest that while the distance to health facilities might influence attrition, it is not a strong predictor within this study.

Accessibility to healthcare facilities remains a crucial factor affecting CBHI program retention. The parameter estimate for the distance to the nearest health facility is 0.730, with a shape parameter (ln(ρ)) of 0.730 and a shape parameter (p) of 2.075, indicating an increasing hazard function over time. The inverse shape parameter (1/p) is 0.482, and the constant is 0.044. The AIC and BIC values are 1354.625 and 1373.221, respectively. Members living 35-60 minutes away from a health facility have a lower likelihood of dropping out (OR=0.83, 95% CI: 0.55-1.11), while those living 70-180 minutes away are more likely to drop out (OR=1.02, 95% CI: 0.73-1.41). These findings highlight the importance of ensuring easy access to healthcare services to reduce dropout rates.

(Figure 12) examines the effect of distance to the nearest health facility on membership retention, categorized into three groups: 5-30 minutes, 35-60 minutes, and 70-180 minutes. Members living 5-30 minutes away from a health facility (curve 1) exhibit the highest survival probabilities throughout the observed period, maintaining a survival probability above 0.7 until the 7th year. This suggests that proximity to healthcare services significantly contributes to higher retention rates, as members can access healthcare more easily and frequently.

Members in the 35-60 minutes category (curve 2) show slightly lower survival probabilities than those living 5-30 minutes away. However, they maintain a survival probability above 0.6 until the 6th year. The retention rate for this group declines more sharply after the 6th year, indicating that while a moderate distance is manageable, it still negatively impacts retention compared to those living closer to healthcare facilities.

For those living 70-180 minutes away (curve 3), survival probabilities are the lowest, dropping below 0.6 by the 4th year and continuing to decline steadily. This group experiences a significant decrease in survival probability over time, indicating higher attrition rates for members living further from health facilities.

The Weibull regression curve analysis highlights that proximity to health facilities significantly impacts CBHI program membership retention rates. Members living closer (5-30 minutes) to health facilities have higher survival probabilities, indicating better retention over the years, with survival probabilities remaining above 0.7 until the 7th year. This underscores the importance of accessibility to healthcare services in retaining members. Members living 35-60 minutes away experience a moderate decline in survival probability, maintaining above 0.6 until the 6th year. Those living 70-180 minutes away have the lowest retention rates, with survival probabilities dropping below 0.6 by the 4th year. This significant drop indicates that the further the distance, the higher the attrition rate.

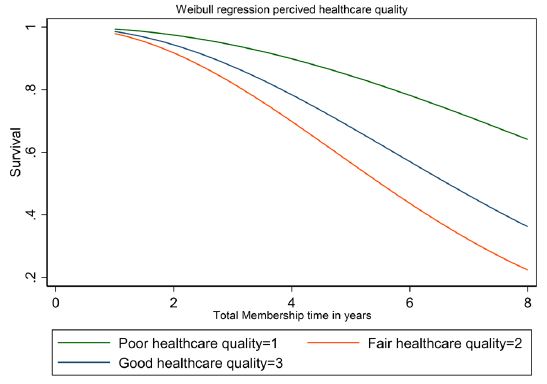

Perceived healthcare quality significantly affects membership attrition within the CBHI program. Members who perceive healthcare quality as fair have a hazard ratio of 1.818 (95% CI: 1.137-2.906), indicating they are likelier to drop out than those with poor perceived quality. Similarly, members who perceive healthcare quality as good have a higher hazard ratio (H.R.=1.887, 95% CI: 1.180-3.018), suggesting that higher perceived quality may raise expectations, leading to dropout if those expectations are unmet.

The parameter estimate for perceived healthcare quality is 0.729, with a shape parameter (ln(ρ)) of 0.729, indicating an increasing hazard function. The shape parameter (p) of 2.074 suggests that the risk of attrition increases over time. The inverse shape parameter (1/p) is 0.482, and the constant is 0.042. The Akaike Information Criterion (AIC) and Bayesian Information Criterion (BIC) values are 1355.329 and 1373.925, respectively. Members who perceive healthcare quality as fair (OR=1.82, 95% CI: 1.13-2.91) or good (OR=1.89, 95% CI: 1.18-3.02) are likelier to remain in the program. This underscores the need for continuous improvements in healthcare service quality to enhance member satisfaction and retention.

(Figure 13) explores the impact of perceived healthcare quality on membership retention by comparing survival probabilities among members with perceptions of poor, fair, and reasonable healthcare quality.

For respondents who perceive healthcare quality as poor (indicated by line 1), the survival probability starts at 1.0 and decreases gradually to about 0.8 by the eighth year. This group shows the highest survival probability throughout the membership period. Respondents who perceive healthcare quality as fair (indicated by line 2) begin with a slightly lower survival probability, around 0.9, which declines more sharply, reaching about 0.5 by the eighth year. Respondents who perceive good healthcare quality (indicated by line 3) have the lowest initial survival probability, starting at about 0.85 and declining steeply to approximately 0.3 by the eighth year.

Members who perceive healthcare quality as poor tend to stay longer, as higher survival probabilities indicate. This counterintuitive result may suggest that those with lower expectations are more tolerant of the program's shortcomings, leading to higher retention rates. Conversely, members perceiving fair or reasonable healthcare quality show lower survival probabilities and higher dropout rates, suggesting that unmet expectations can lead to dissatisfaction and early departure from the program. The steepest decline is observed among those who perceive good healthcare quality, indicating that unmet high expectations could drive membership attrition.

Service quality is another crucial factor affecting retention. Members who perceive service quality as satisfactory have a higher hazard ratio than those who perceive it as excellent (H.R.=1.264, 95% CI: 0.916-1.745). Poor service quality does not significantly affect attrition (H.R.=0.955, 95% CI: 0.660 - 1.381). Improving perceptions of service quality could reduce dropout rates.

The parameter estimate for service quality is 0.730, with a shape parameter (ln(ρ)) of 0.730 and a shape parameter (p) of 2.075, indicating an increasing hazard function. The inverse shape parameter (1/p) is 0.482, and the constant is 0.043. The AIC and BIC values are 1355.523 and 1374.119, respectively. Members who rate service quality as satisfactory (OR=1.27, 95% CI: 0.92-1.75) or poor (OR=0.96, 95% CI: 0.66-1.38) have varied retention likelihoods. These findings underscore the importance of maintaining high service quality standards to ensure member retention.

The analysis in (Figure 14) evaluates how perceived service quality-categorized as excellent, satisfactory, and poor-impacts survival probabilities in the CBHI program. Members who perceive service quality as excellent show the highest survival probabilities, with gradual declines over time, indicating strong retention rates. Specifically, these members have survival probabilities of approximately 0.95 after two years, 0.85 after four years, 0.75 after six years, and 0.65 after eight years.

Members perceiving satisfactory service quality have moderate survival probabilities, with a curve between excellent and poor service quality. Their probabilities are around 0.90 after two years, 0.75 after four years, 0.60 after six years, and 0.50 after eight years.